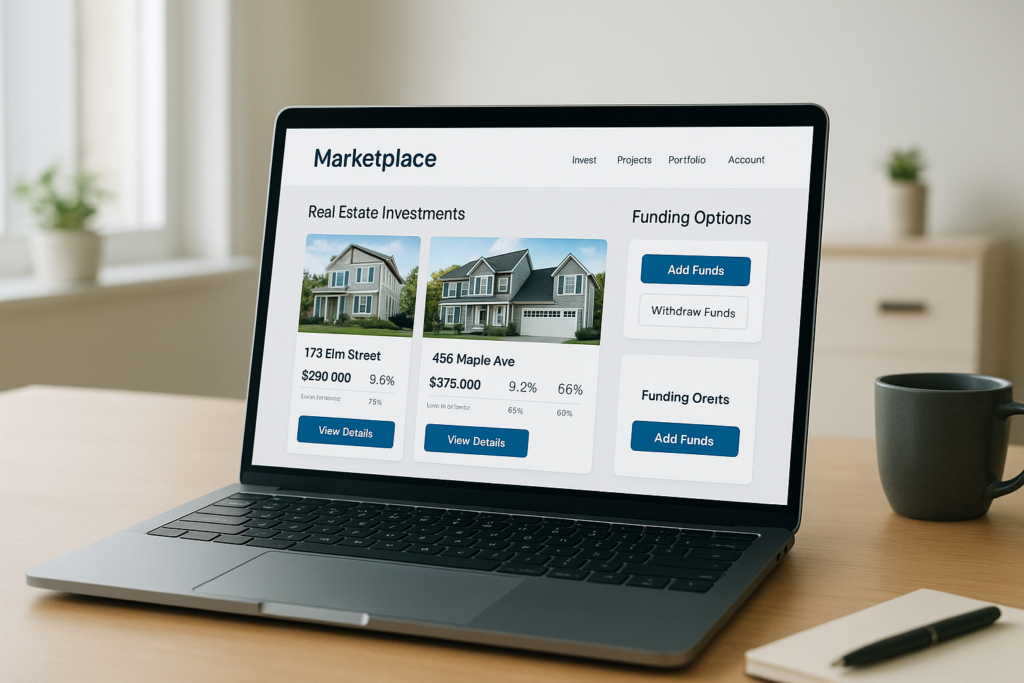

Private Money Investment Opportunities: Find & Compare Deals

Private Money Investment Opportunities: Find & Compare Deals Private money investment opportunities give real estate investors and lenders a way…

Read More